.png#keepProtocol)

Table of Contents

abluecup

Icahn Enterprises (NASDAQ:IEP) is a diversified holding company controlled by billionaire investor Carl Icahn, known for his activist campaigns involving several high-profile companies. Mr. Icahn has been actively involved in advocating for changes at various companies. One of his latest endeavors involves a proxy battle with Illumina Inc (ILMN), in which he is urging the U.S. life sciences company to reverse its acquisition of Grail in 2021. Turning the tables around for a change, Icahn Enterprises has become the target of a scathing report by Hindenburg Research, a short-seller with a reputation for exposing fraud and accounting malpractices. After reading Hindenburg Research’s short thesis on Icahn Enterprises, I thought IEP investors would find interest in a summary of the key points raised by Hindenburg. In this article, I will summarize the key takeaways from the short report while giving more color on some points.

Key Takeaways

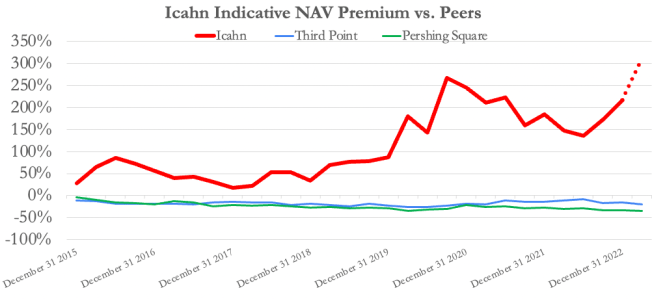

Hindenburg Research published a report on May 2, 2023, accusing Icahn Enterprises of being overvalued and operating a “Ponzi-like” business. The report claims that IEP’s units are inflated by more than 75% due to questionable valuations of its holdings, especially its energy and real estate segments. IEP also trades at a premium to its net asset value, while its peers, like Dan Loeb’s Third Point and Bill Ackman’s Pershing Square, trade at a discount. All these investments are closed-end funds and cannot be redeemed by investors. Hindenburg claims that both Third Point and Pershing Square might charge high fees which could be the reason why their investments are traded at a discount to their NAV. On the other hand, Icahn’s closed-end fund may charge lower fees than its peers, but it is currently trading at a premium of about 218% to its NAV as of December 2022. This premium was compared against all 526 closed-end funds listed in Bloomberg’s database, and IEP’s premium was found to be the highest – more than twice as high as the premium of the second most expensive closed-end fund.

Exhibit 1: IEP’s NAV premium vs peers

Hindenburg Research

Hindenburg also alleges that IEP has been selling new units to fund the dividend payouts, creating a “circular” and unsustainable economic structure. This reliance on selling new units erodes IEP’s net asset value over time. IEP’s public market investment portfolio has underperformed since 2014, losing 53% while the S&P 500 gained 147% in the same period. The report further highlights that IEP has posted $4.9 billion in free cash flow losses since 2014 due to portfolio losses and declines in IEP’s operating investments. However, the company has continued to pay unitholders cash dividends of almost $1.5 billion during this period and even raised its quarterly dividend three times. In the past four years alone, IEP has paid out $980 million in cash dividends, despite burning almost $1.6 billion in free cash flow. The company has supported its dividend and declining asset values by $1.7 billion worth of at-the-market unit sales over the past four years.

Hindenburg Research wrote:

Icahn has been using money taken in from new investors to pay out dividends to old investors.

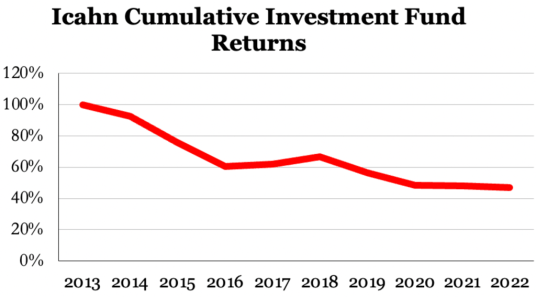

Exhibit 2: IEP’s cumulative returns

Hindenburg Research

While Icahn’s investment fund outperformed the market in 2013, returning 30.8% and coinciding with the start of his successful Herbalife Campaign, his recent performance has suffered. Hindenburg’s allegations raise concerns about IEP’s long-term viability, as its reliance on selling new units to fund dividend payouts may cause its net asset value to erode more over time.

Hindenburg’s report gives examples of IEP’s holdings in Viskase Companies Inc. (OTCPK:VKSC) and its automotive parts division to establish some of the points raised in this report. IEP valued its 90% stake in Viskase at $243 million in December 2022, despite the market value of the company being only $88.7 million. IEP attributed this to the lack of trading volume in Viskase’s shares. Additionally, IEP marked up the value of shares it bought in Viskase by almost 194%, despite the public market price remaining flat. Further, despite Viskase’s earnings being only $2.2 million in 2022 and net losses coming to $3.3 million in 2021, IEP valued its stake on a 9x adjusted EBITDA number. Hindenburg believes that IEP’s portfolio valuations are way above their market value and that they should have applied a significant liquidity discount in both instances.

On the other hand, IEP’s automotive parts division was valued at $381 million in December 2022, just a month before a key subsidiary of the division filed for bankruptcy. The division includes Auto Plus, which is described as a “leading after-market parts distributor”. The bankruptcy filing showed $238 million in creditor claims, indicating significant indebtedness. This suggests that IEP’s $381 million valuation will be written down significantly in the coming months.

Hindenburg claims that Jefferies & Co., a financial services company, is the only sell-side analyst covering IEP and has assumed in its research notes that IEP’s dividend is safe in perpetuity, despite its extended period of losses and negative cash flow. Carl Icahn has a long-standing relationship with Jefferies. In the 1970s and 1980s, he allied with Boyd Jefferies, the founder of Jefferies & Co., and together they challenged Wall Street by buying stakes in undervalued companies and pushing for changes that would boost their share prices. Mr. Icahn and Mr. Jefferies were both part of a network of alliances and rivalries among corporate raiders during this time. One of Mr. Icahn’s notable allies was T. Boone Pickens, and they collaborated on several high-profile takeovers. Carl Icahn’s most famous deal at the time was his takeover of Trans World Airlines in 1985. He eventually became its chairman and chief executive, but his reign was controversial and turbulent.

Boyd Jefferies, on the other hand, helped facilitate some of the biggest corporate takeovers in the U.S. However, he was involved in illegal activities such as parking stocks for Ivan Boesky, a notorious inside trader. Mr. Jefferies pleaded guilty to two counts of securities fraud in 1987, cooperated with the government in several cases against other Wall Street figures, and was fined $250,000 and sentenced to five years of probation.

In 2011, Jefferies & Co. faced a liquidity crisis as its bonds plummeted in value due to market fears over its exposure to European sovereign debt. In a surprising move, Mr. Icahn stepped in and bought a large amount of Jefferies bonds, effectively rescuing the firm from potential bankruptcy. Given this history, Hindenburg alleges that Jefferies has helped Icahn by issuing bullish research reports on IEP and selling its stock to retail investors. The firm argues that Icahn’s empire is crumbling under the weight of its debt and losses and that it is relying on selling overpriced IEP units to unsuspecting investors while promising them a safe and consistent dividend.

UBS Group AG (UBS), a multinational investment bank, stopped covering IEP in January 2020 due to concerns over transparency, discrepancies in IEP’s portfolio valuation techniques, and investment underperformance. Before that, UBS was the only other large bank aside from Jefferies that covered IEP. UBS analyst Brennan Hawken had a sell rating on IEP’s units because of its lack of transparency. In 2017, UBS noted that IEP’s Tropicana and Viskase holdings had irregularly high reported values because IEP did not use public market prices. Hawken wrote that the carrying values of Tropicana and Viskase remained distant from their public market values. In January 2020, Hawken cited IEP’s lack of transparency, marginal private subsidiary performance, and a 60% premium to NAV as reasons for dropping coverage.

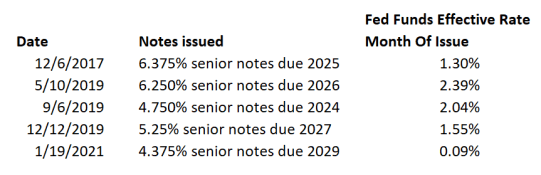

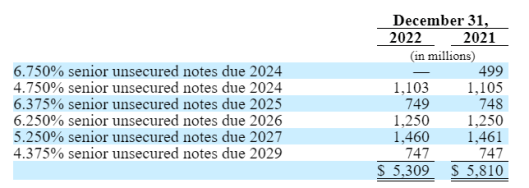

The Hindenburg report also highlights that IEP has been experiencing weakening performance causing concerns among creditors. Since 2015, IEP has not been allowed to take on additional debt, and its recent 2022 annual report reiterated this restriction, noting that the company can only refinance existing debt. As of December 2022, IEP had long-term debt of over $7 billion and $2.3 billion in cash and short-term investments. Some of the company’s debt was issued at historically low interest rates between 2017 and 2021. As this debt approaches maturity, refinancing may result in significant interest expenses for the company. Additionally, Mr. Icahn has pledged 60% of his IEP units for margin loans, which is a risky form of financing that could result in margin calls if unit prices decline. However, Mr. Icahn has not disclosed the key terms of his margin loans, which makes it difficult for unitholders to fully understand and quantify this risk.

Exhibit 3: IEP’s current debt

Hindenburg Research

Exhibit 4: IEP’s debt maturity profile

2022 Annual Report

Hindenburg Research wrote:

We think Icahn, a legend of Wall Street, has made a classic mistake of taking on too much leverage in the face of sustained losses: a combination that rarely ends well.

The impact of Hindenburg’s report was significant, as IEP’s shares dropped by more than 20% on Tuesday, erasing $2.9 billion from Mr. Icahn’s net worth. (**Editor’s note- IEP’s shares fell 19.3% on Wednesday.) This represents a rare challenge for Carl Icahn, who is one of the pioneers of shareholder activism and has often criticized other companies for their governance and transparency practices. Mr. Icahn rejected Hindenburg’s allegations and called the report “self-serving” and accused Hindenburg of trying to profit from its short position at the expense of IEP’s long-term shareholders.

Icahn Enterprises defended IEP’s performance and transparency saying:

We stand by our public disclosures and we believe that IEP’s performance will speak for itself over the long term as it always has.

Conclusion

The Hindenburg short report accusing Icahn Enterprises of being a “corporate raider” and engaging in dubious accounting practices has sparked a heated debate among investors and analysts about the true value and prospects of the company. While some may view Icahn Enterprises as a risky and overvalued investment that relies on the reputation and influence of Carl Icahn to attract capital, others believe it is an undervalued conglomerate that benefits from Mr. Icahn’s expertise and activism.

At Beat Billions, we keep a close eye on investing gurus and their investments to find stocks that pass our screening criteria. Our investment strategy is centered around earnings revisions, earnings surprises, and the stock price sensitivity to these events. With just one Wall Street analyst covering IEP, the company certainly does not meet our investment selection criteria.

.png#keepProtocol "The Key to Boosting Retention")

More Stories

‘The Forest Must Stay!’ Treetop Protest Erupts At Tesla’s Berlin Gigafactory As Activists Try To Thwart Expansion – Tesla (NASDAQ:TSLA)

GamerSafer acquires Minecraft-focused Minehut server community

New York Appeals Court allows Trump, sons to continue running business, denies request to delay payment